-

Your trusted market research partner

- info@theindiawatch.com

- 8076704267

Demand for Solar Panel set to grow in India

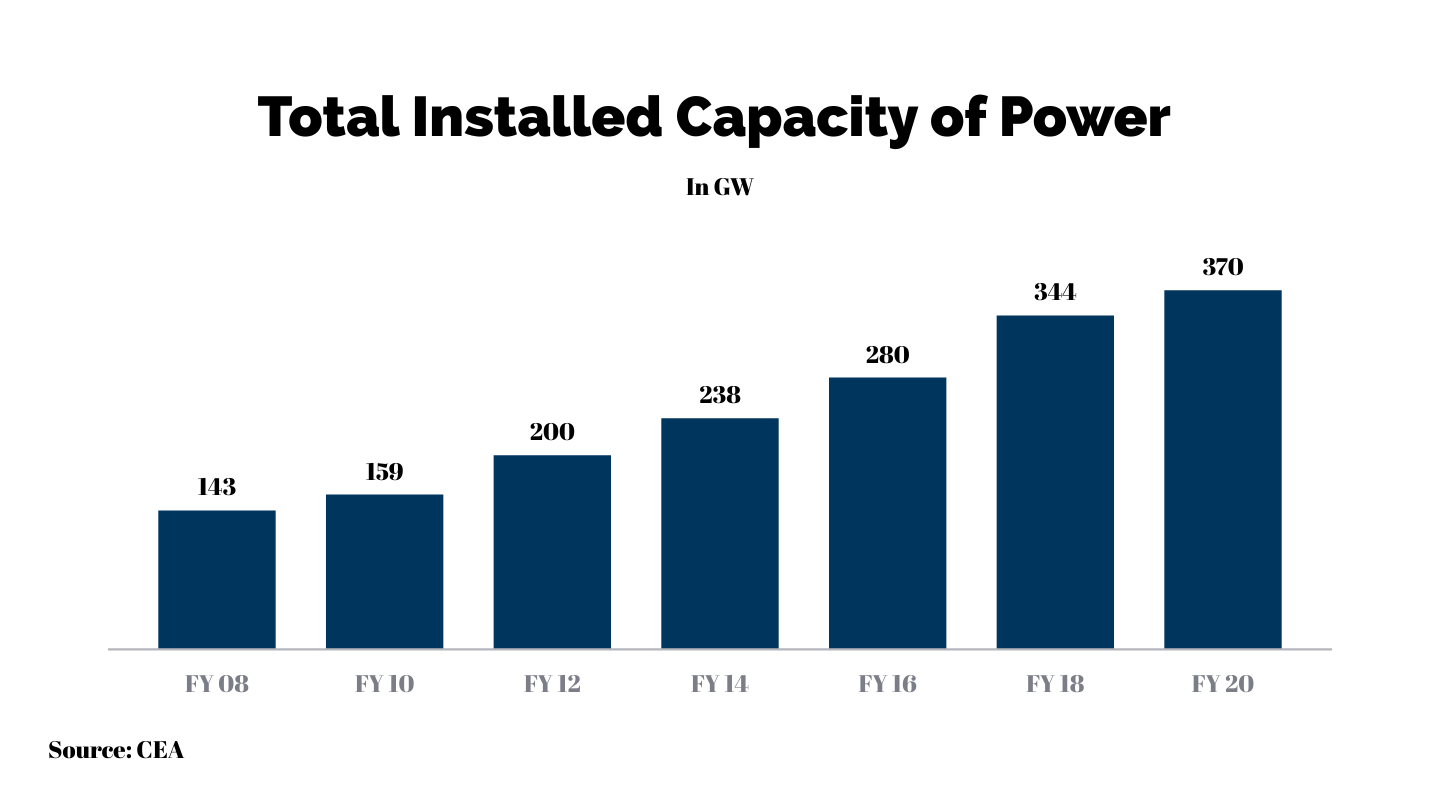

As an emerging economy, India understands how energy can become an iron pillar to fuel its growth ambitions. With an installed capacity of 372 GW, India is the world’s 3rd largest producer and consumer of electricity.

India’s energy roadmap is also pinned on its commitment to reduce overall CO2 emissions and focus more on renewable energy. The government directive aims at renewable sources contributing to around 40% of the overall power generation. Currently, renewable constitutes 22% of the aggregate power generation.

Out of the various sources, solar plays an important role in a land, which has abundant sunlight throughout the year. The total installed capacity of solar energy has reached 36 GW in 2020, growing at a CAGR of 51.7% in the past 4 years. Besides, there is around 40 GW of capacity under construction. Although the country will fall short of the stipulated target of 100 GW of installed solar power by 2022, its objective by producing clean solar energy will continue undeterred.

As the country is aggressively expanding solar energy generation capacity, the demand for solar panels has sharply risen over the years.

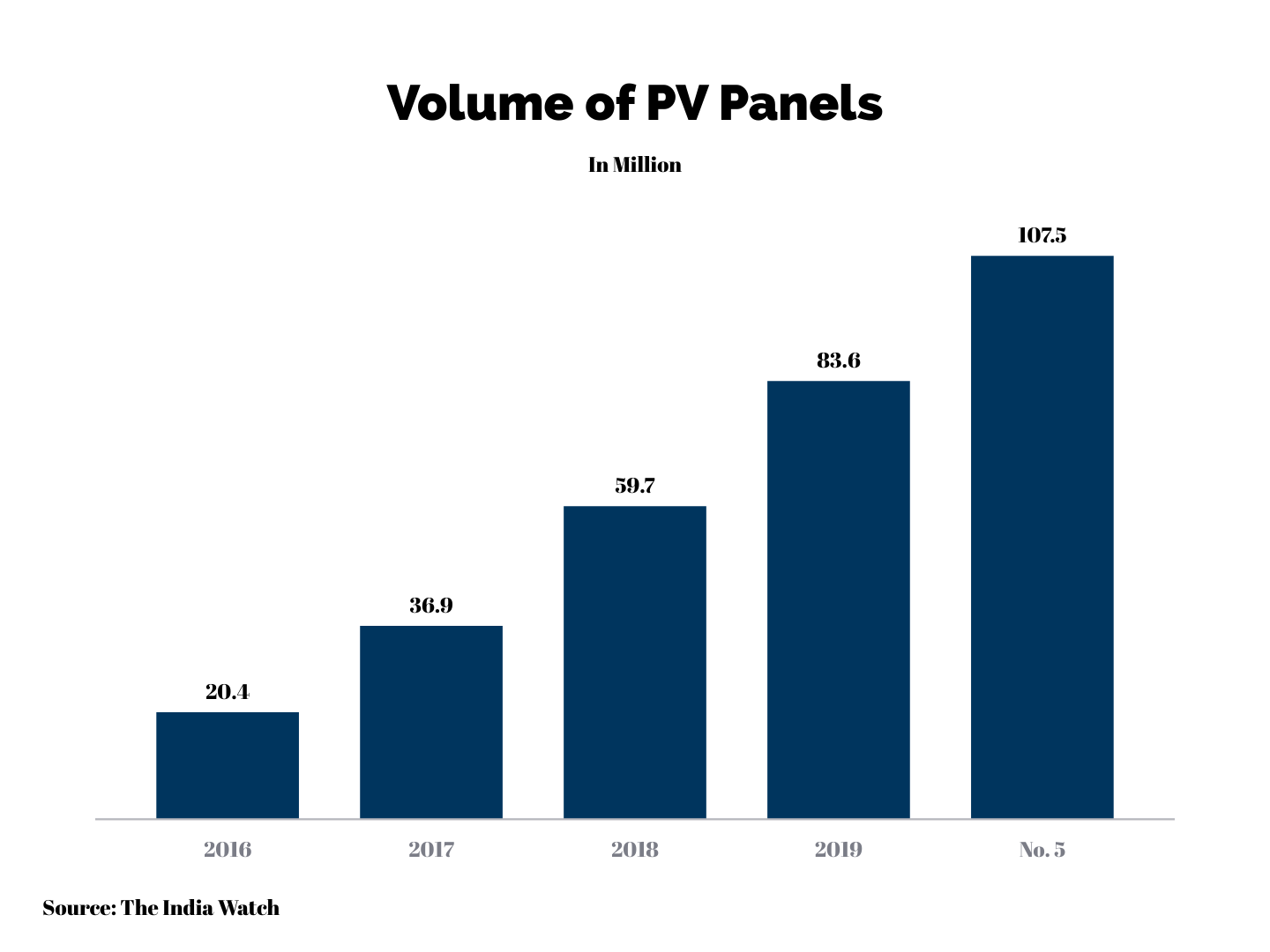

As of 2020, the market size of PV panels in India is estimated at around USD 15 billion, growing by 28% in the last 12 months. In the past 4 years, the market size of solar panels in India has grown fivefolds.

Around ~ 85% of the solar panel market is utility type while the remaining ~ 15% is rooftop based. Major corporates active in the manufacturing of solar panel in India include Vikram Solar, Waree energies, Tata Power Solar, Mosarbear solar ltd, XL energy Ltd, Alpex Exports, Renew Sys India Ltd, Emvee photovoltaic, Lanco Solar, Saatvik Green energy, JA Solar, Canadian Solar, and Trina Solar, etc.

India’s leading business house Adani has been recently awarded one of the largest solar energy contracts in the world. It has been awarded by the Solar Energy Council of India (SECI) to build 8 GW of solar power capacity, with an additional contract to develop solar panels equivalent to 2 GW of power.

Growth Drivers of Solar PV in India

- India currently has a solar energy capacity of 36 GW with an additional 40 GW under various construction. As solar energy will climb sharply, the demand for solar panels will continue to get a positive boost.

- Although Chinese (alongside Malaysian and Vietnamese) products have a strong foothold in the market, numerous domestic players are also ramping up their capacity fast.

- The governments and regulatory bodies alongside corporates and businesses understand the significance of lowering the reliance on conventional sources of energy by enhancing renewable production capabilities.

- 100?I is allowed under the automatic route for solar energy in India. The country has received over USD 6 billion of FDI from FY 14 to FY 20.

- To clamp down on Chinese imports, a safeguard duty of 25% was imposed on solar panel imports from China.

- India has deepened its foothold across the solar energy value chain which also includes enhanced capacity in the solar inverter, mounting structures, solar gridlines manufacturing.

- The cost of solar energy production has reduced drastically over the years. In 2010, the cost of producing 1 KW of solar energy was INR 17. Currently, it has come down to INR 2.44.

Headwinds in Indian Solar Industry

- China still accounts for around 80% of Indian imports of solar panels. Chinese products are believed to be 6-8% cheaper when compared to their domestic peers.

- India needs an investment of USD 100 billion to completely harness and utilize its solar energy potential. The current investments through the FDI route are relatively less. As in a post-COVID world, the lending capacity of domestic banks has also weakened, the country needs to develop other innovative funding mechanisms.

- Systematic Investments and impetus is required in R&D facilities.