-

Your trusted market research partner

- info@theindiawatch.com

- 8076704267

In a Tea Drinking Nation, Coffee Retail has Enough Potential to Grow

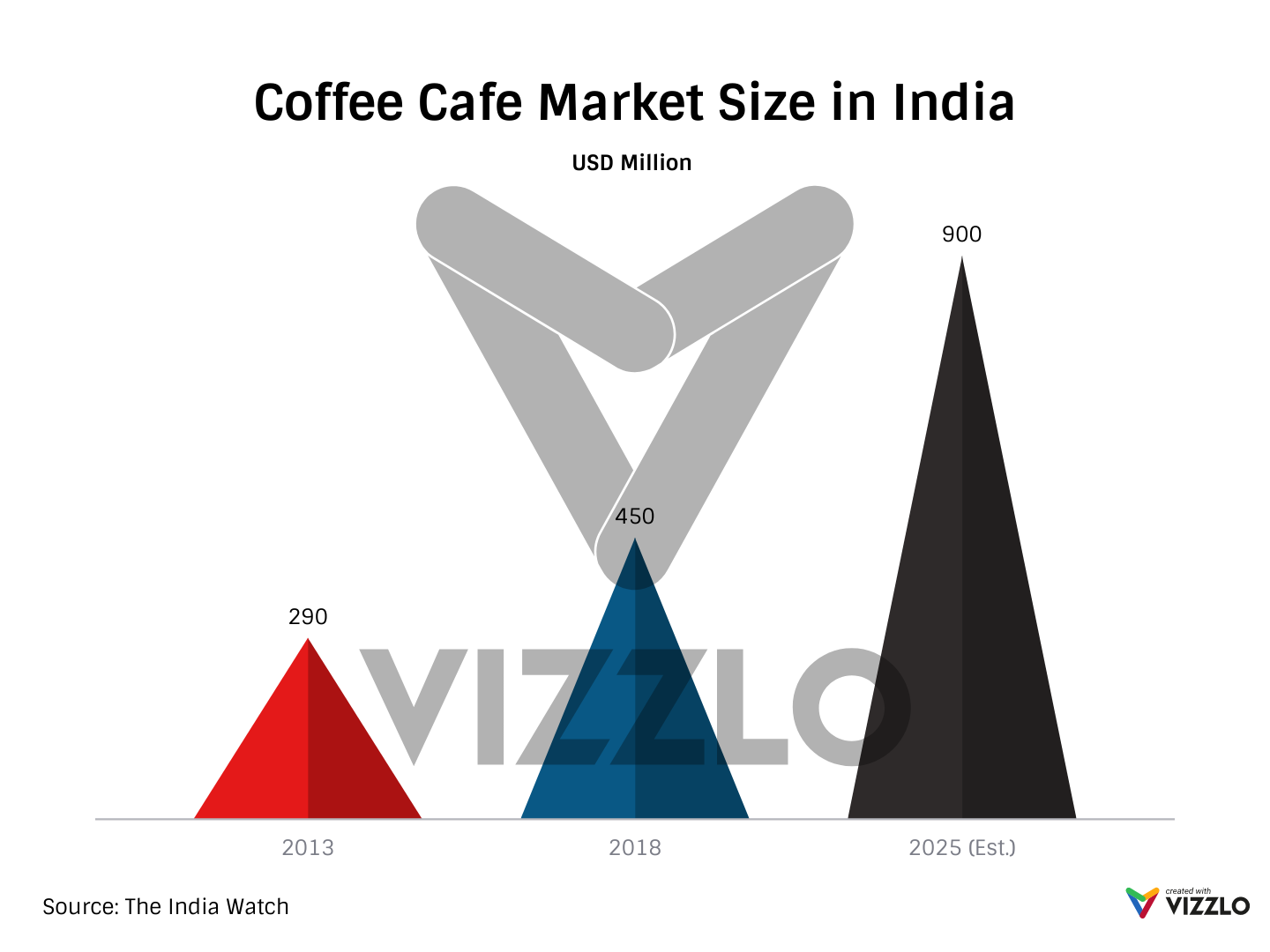

Slowly and gradually Coffee Café Chains are gaining ground in India. As disposable incomes are rising, Indians are willing to spend more on entertainment, experiences, & leisure. The current size of coffee chain market is pegged at around USD 450 million. However, it is expected to double by 2025.

India is traditionally a tea-sipping country, where the per capita consumption of coffee is roughly just ~ 100 gm- far behind the USA (4 KG), Finland (9 KG), and France (5 KG). However, as consumption trends are altering, domestic and international coffee retail brands have ample space to flourish.

The country is gradually shifting towards consumption-driven culture. As the size of affluent & middle class is rising in India, consumer behavior is also changing. Though a lot of Indian middle class still prioritizes savings, they are willing to spend more on entertainment, socialization, & comfort.

Places like coffee outlets are increasingly becoming popular for individuals to interact & socialize. Urban Indians are now willing to spend USD 4-7 on a cup coffee along with some snack items. Twenty years back, this might would have been a rare phenomenon.

In the times ahead, F&B outlets such as coffee cafes will continue to gain ground. The rising number of malls & highstreet retail will also fuel growth. Other factors such as the growing volume of freelancers (many of whom operate from coffee cafes) and a rising preference for non-carbonated drinks will also help in driving growth.

Coffee Café Market in India

In 2018, the total size of the coffee café market in India reached USD 450 million, recording a CAGR of 9.2% in the last five years. In the next 7 years, the market is expected to double in size, growing by a CAGR of little less than 15%.

Currently, the domestic brand Café Coffee Day (CCD) dominates the market with near around half of the share. CCD was originated in Bangalore in 1996 and since then has proliferated all across the country including smaller towns. It is credited for being the pioneer of coffee culture in the country. CCD is available across high streets, shopping malls, transport hubs, educational institutes, corporate parks and much more. Its success in the Indian market has been underpinned by 3A strategy- Affordability, Accessibility, and Acceptability. Its offerings are priced in the way that it goes well with the emergent yet price-conscious Indian middle-income segment. It has an extensive reach & is available across places with higher footfalls. Lastly, the outlets are designed to give enough privacy and comfort without disturbance, something that average visitors are looking forward to.

Starbucks, which entered the Indian market in 2012 is the distant second The global giant, which has partnered with Tata has posted a revenue of over USD 50 million in FY 2017-2018, growing 28% Y-o-Y.

However, Starbucks is not the 1st international coffee café chain that entered the Indian market. In 2005, Costa Coffee forayed into India. By 2013, it had over 100 outlets. However, since then more than half of the outlets have to be shut down, as the brand is yet to make any substantial profit in the country.

The Marker has Enough Potential to Grow

Coffee Café chain markets have enough potential to thrive in India. As disposable incomes amongst Indians will rise & appetite for quality experiences will grow, the demand for cozy & comfortable food & coffee cafes will rise. The Government has also allowed 100% FDI in food retail that will further draw the attention of international brands. Apart from the rise in demand, café operators can also draw upon cheaper rentals & labor charges to grow their yields.

Retail rentals rates have grown significantly in recent years in Indian metros, yet there is a marked difference when compared to other cities in the emerging world. Likewise labor costs are relatively much cheaper in India. This will give additional impetus to global & indigenous brands to contain their costs and post better margins.

However, a complex, heterogeneous, & emergent markets like India has its challenges. The coffee café culture is still in its nascent phase and brands will take time to grow and make profits. In India, there is very little coffee takeaway culture, as people mostly prefer to visit café and spend time. The average table-turnaround time is generally around 1- 1.5 Hr, which affects profitability.

Despite major makeovers in the consumer landscapes, Indian consumers continue to be value-driven and price sensitive. Brands that have understood it in the past & accordingly worked on their business strategies have grown. While others have staggered.

About The India Watch

The India Watch is an India based market research and business intelligence agency. We have in-depth expertise in devising India's market entry, evolution, & growth strategy. If you are looking for research and advisory services in the retail segment, feel free to connect with us by dropping a mail at Info@theindiawatch.com

We can render you usable insights & information on market size, market growth, customer assessment, competition, value chain, distribution structure, & much more.

Rise of Coffee Retail Real Estate in the Country

India is mostly a tea drinking nation.

Highest sales €“ Cappuccino (40%), latte (30%), Black Coffee/ Expresso (20%), others (café latte, café mocha, Americano, 10%).